As usual, I was browsing the new lows list and noticed that Coca-Cola Hellenic (CCH) was hitting new lows every day. Well, of course it's hitting new lows every day. This is a Greek company. But since it kept hitting new lows every single day, I decided to take a quick look as I really haven't looked very hard in Europe despite the meltdown going on over there.

First of All, Is it Cheap?

CCH is trading now at $15.30 or so compared to a high of close to $50 back in early 2008, so the stock is down close to 70% from it's high, and it's not even a bank stock.

But nominal price is not meaningful at all, of course. So let's look at some comparisons.

Here's a quick look at CCH versus other Coke bottlers around the world (I exclude Japanese bottlers here as they seem to live in a different world altogether):

ttm = trailing twelve months through September 2011

Operating margin and ROE are also based on trailing twelve months.

Data is from Yahoo Finance

From the above table, we see that CCH is indeed cheap especially based on next year's earnings estimate trading at 11.6x p/e versus 16.5x and 17.2x for Femsa and Amatil. CCE is cheaper at 10.8x p/e, but CCE's markets are primarily mature markets in Western Europe (Belgium, France, Great Britain, Luxembourg, Monaco, Netherlands, Norway and Sweden) so their growth prospect is not that bright (it can still be a great investment here if they focus on returns on capital and returning cash to shareholders etc...).

Coca-Cola Amatil is the Australia/New Zealand bottler. They have done well with very good margins, return on equity and decent growth but they are not particularly cheap. Again, this is not to say that's a bad investment; we are just comparing things to CCH. I haven't taken a close look at CCLAY.

Coca-Cola Femsa, of course, is the star of the the bottlers with decent margins and plenty of growth (sales have grown +15.5% in the last five years); a perennial favorite of fund managers around the world.

But if you look at CCH, even though their ROE and operating margin is a little depressed due to the current weakness in their European markets (they typically earn an operating margin closer to 10% and return on equity well into the double digits), it does seem to have good growth prospects compared to CCE.

CCE Was a Growth Stock

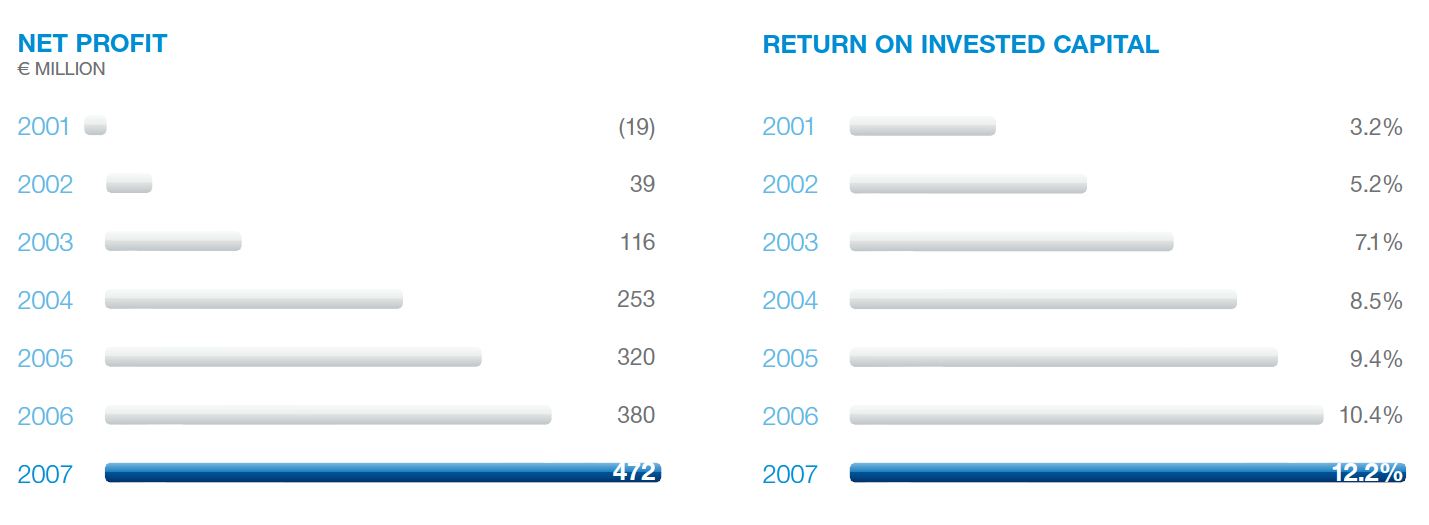

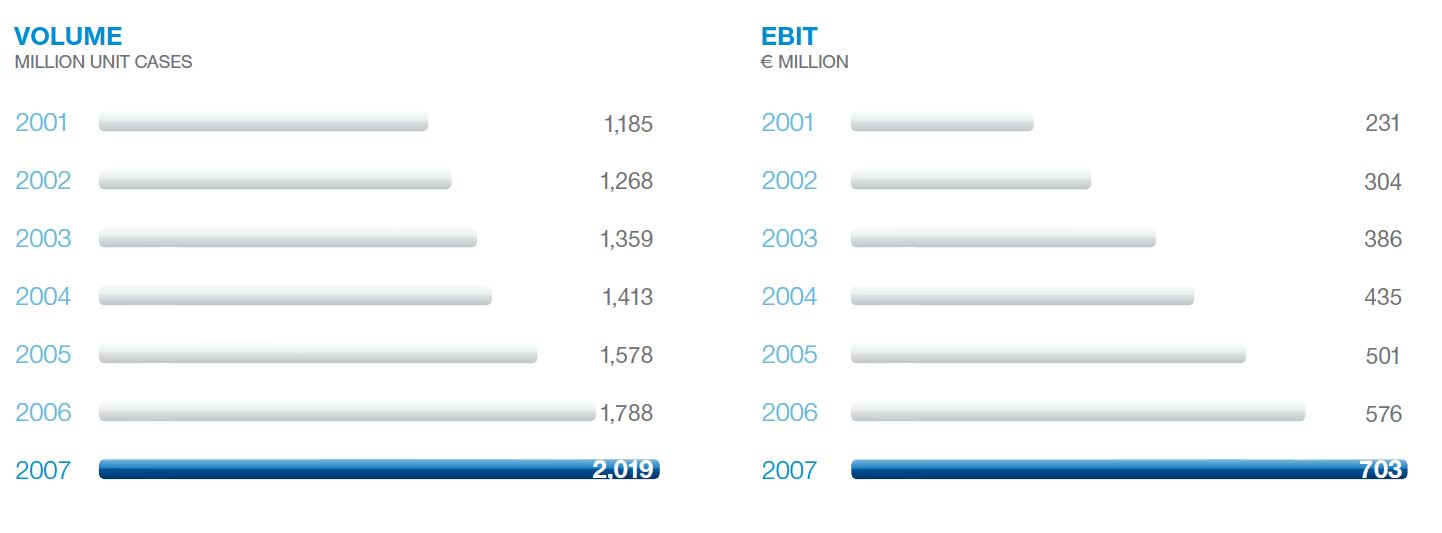

After the merger that created CCH (Hellenic Bottling and Coca-Cola Beverages) in 2000, CCH had a nice run of growth until the financial crisis hit.

Between 2001 and 2007, unit case volumes increased +9.3%/year, revenues grew 11%/year, EBIT grew +20%/year and EBITDA grew 13.6%/year. Return on capital improved over time from 3.9% in 2001 to 12.2% in 2007.

Here are some charts that show nice growth and operational improvements between 2001 and 2007 (this is from the 2007 annual report):

It shows nice growth between 2001 and 2007. Then the financial crisis hit and things flattened out. On back of this growth, in early 2008, CCH stock traded close to $50/share. EPS in calendar 2007 was US$1.90/share so that's a P/E of 26x. Not cheap.

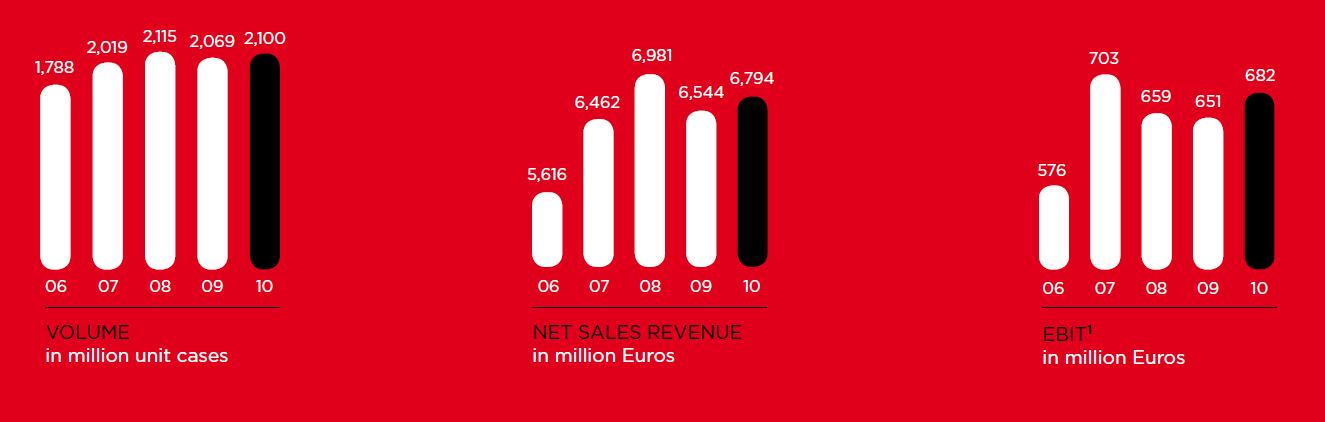

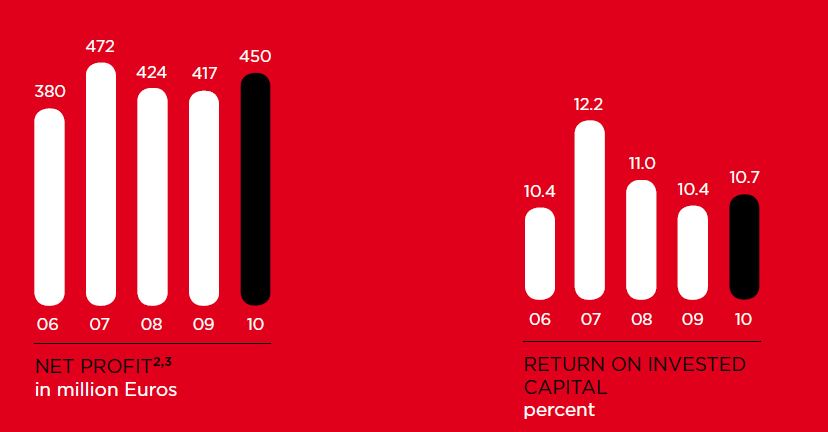

Here are some snips from the 2010 annual report:

Things have flattened out since 2007-2008, but CCH has maintained their return on invested capital and margins at least through 2010. This year, volumes are flat and earnings are down but that's no surprise given the crisis occuring in Europe now.

The question is if this slowdown and ongoing European crisis is a temporary thing or a permanent one. If it's permanent and you think Europe and especially the smaller economies will go into a long depression, then CCH is obviously not a good idea.

But if you think over time that GDP per capita will continue to go up over time, this is an interesting play.

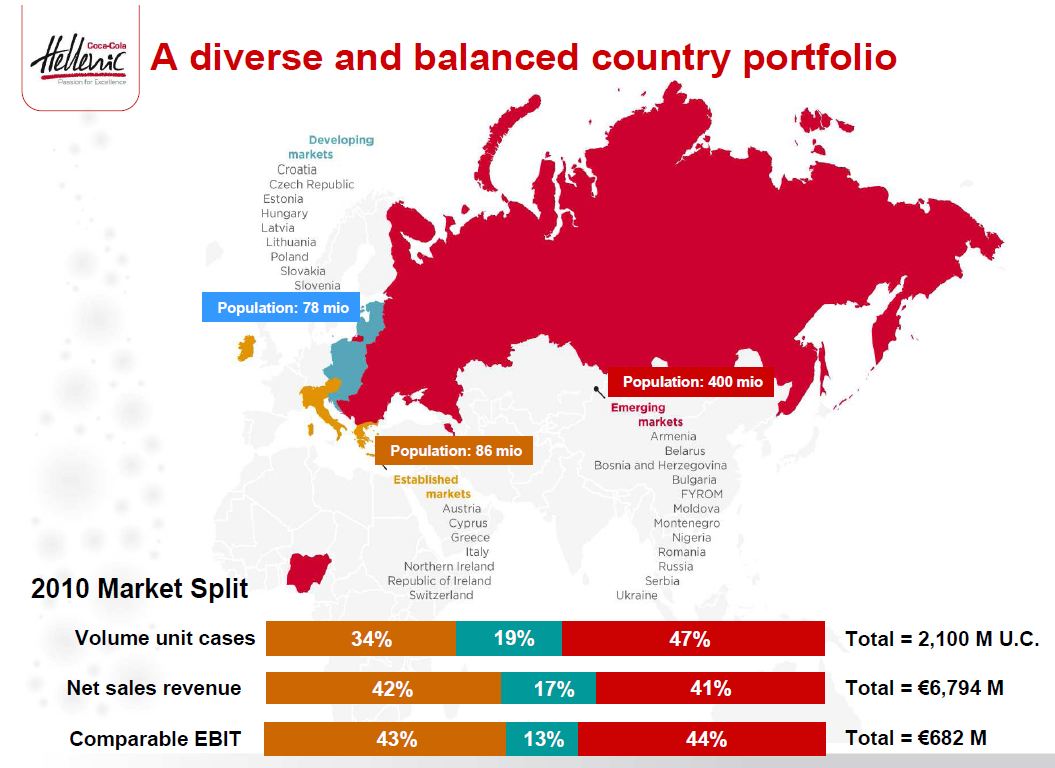

Let's take a look at some of the markets CCH is involved in:

This is actually a pretty impressive portfolio; only 34% of volume and 42% of revenues come from mature markets and the rest from emerging and developing markets. Some of these markets are markets where people were falling over themselves trying to get equity exposure; emerging market funds etc... (remember "frontier market" funds?) There seems to be plenty of potential for growing per capita GDP in many of these markets, and Coca-Cola consumption tends to rise as GDP per capita rises.

Here is a great graph illustrating that from CCH's 2010 annual report:

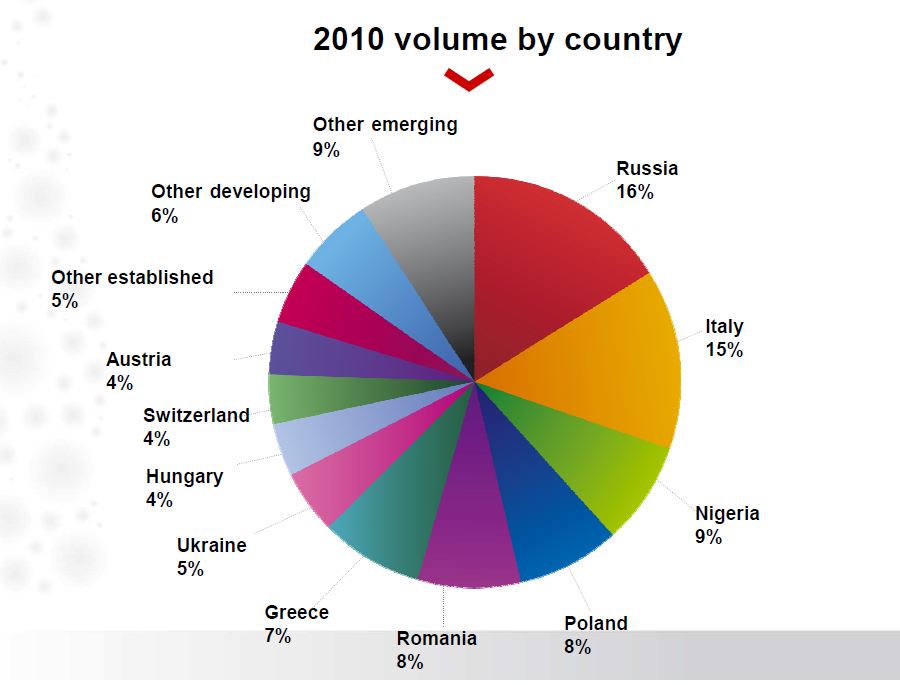

For those worried about specific country exposure (some don't want anything to do with Russia, Italy, Greece etc...), here is a breakdown of the largest sales by country:

Again, this is certainly an interesting portfolio compared to other bottlers in mature markets. Of course that also means there are a lot of risks here.

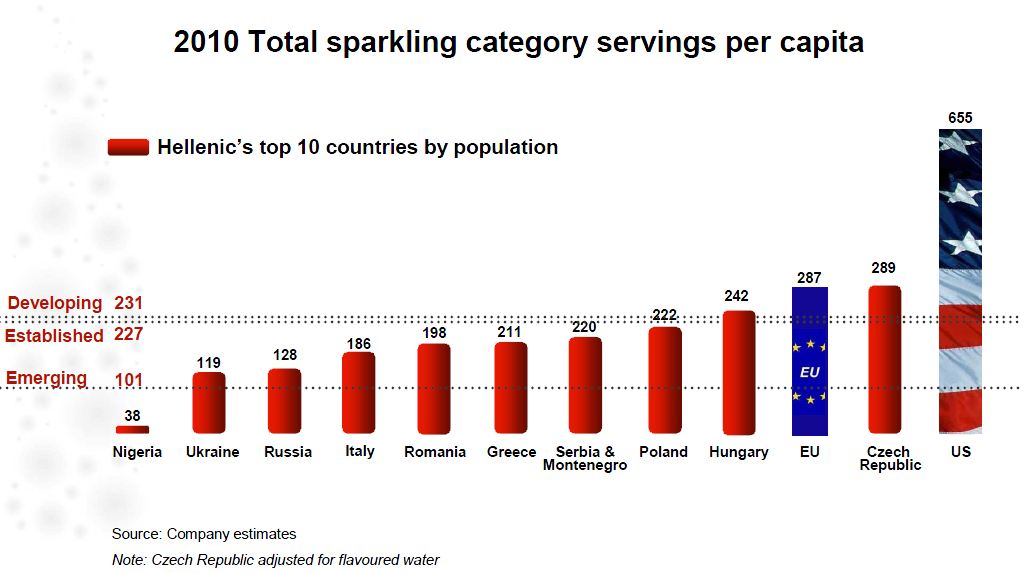

Here's a look at per capita carbonated soft drink (CSD) consumption per capita in CCH's ten largest markets compared to the EU (Eurpean Union) and U.S. averages:

Of course it would be silly to assume that the rest of the world would increase CSD consumption per capita to U.S. levels, but it wouldn't be unreasonable to assume that many of these markets might move closer to the EU average. Of course, in mature markets where Coke has had a long presence and GDP per capita has been stable over time, I doubt CSD per capital figures would grow much, but for countries with low GDP per capita, I find it totally reasonable to assume CSD per capita figures will grow with GDP per capita.

So What's CCH Worth?

The above table shows the return on equity of CCH over the past decade; I just divided the net profit of the year by the shareholders equity at the beginning of the year. I also calculated the EPS over the past decade in U.S. dollars. I translated the Euro into U.S. dollars using the currency exchange rate at the end of each year.

So we see that this stock that traded near $50/share at 26x p/e is now trading at less than 10x what they earned in both 2009 and 2010, and 11.6x or so of what analysts expect them to earn in the year ended December 2012. This seems to me a very reasonable valuation.

A lot of growth stocks come crashing down from a high p/e ratio to a ratio that would attract value investors (like me), but many of those come down due to limits on their growth due to market saturation (fast food restaurants etc...), technological obsoletion (new technology obsoleting products and services), end of fads (Heelys etc...) and sometimes things just come down due to temporary macro problems.

CCH might fall in the category of this 'temporary' problem. I don't think CCH fits into any of the other categories. Is there a secular change in this business, technological or otherwise? I don't think so. I don't know if CCH actually deserves to trade all the way up at 25x p/e either, but 10x might be a bit cheap for a company that seems to have so much growth potential going forward with a proven business model that works and has worked over many years. Their business model is also supported by a globally dominant company that has an interest in seeing them succeed. That's pretty important, especially when looking for exposure (for investors) in some of the smaller more obscure markets.

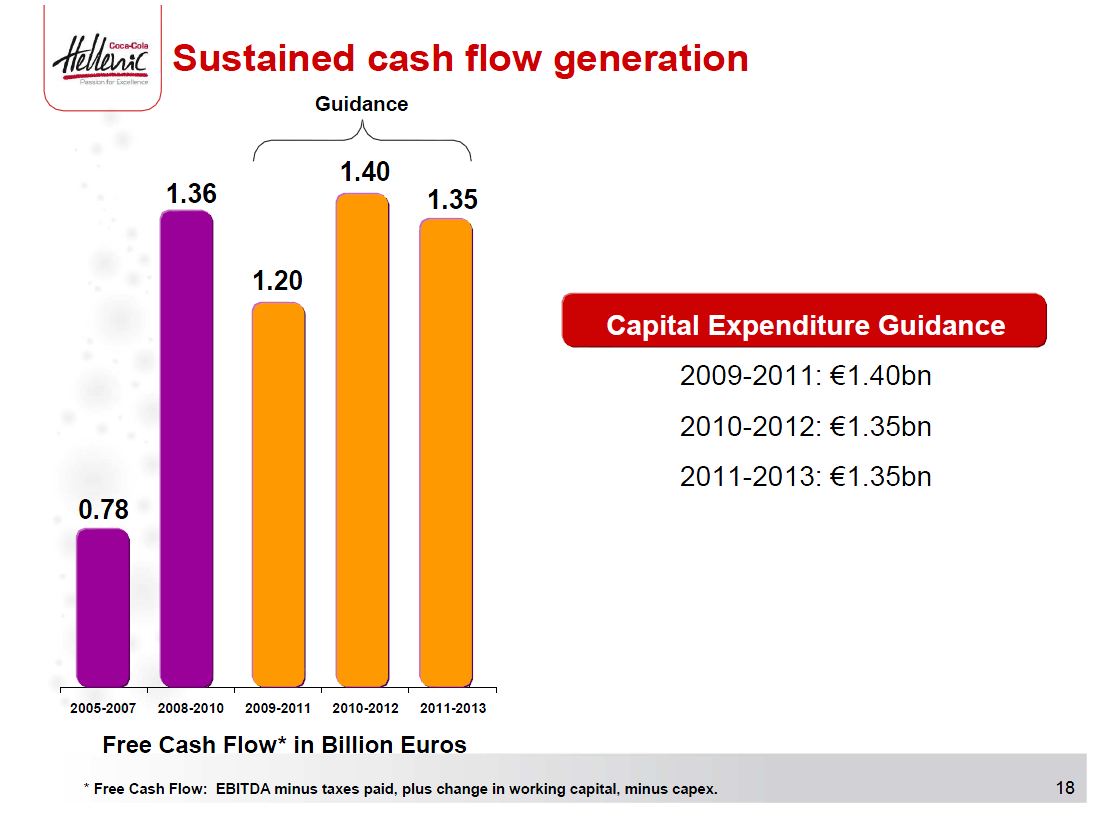

Free Cash Flow

Let's look at free cash flow. CCH provided their own free cash flow calculation and forecast in the November presentation:

This cash flow doesn't deduct interest expense, so either we have to look at this versus enterprise value (EV), or deduct some sort of interest expense to compare it to the equity (stock) valuation.

First, let's look at this versus the enterprise value.

The stock is now trading at around 11.4 Euros/share and there is around 366 shares outstanding for a market capitalization of 4.2 billion Euros. Non-current liabilities on the balance sheet as of September 2011 was 2.4 billion Euros for a total enterprise value of 6.6 billion (out of conservatism, I won't deduct the cash on the balance sheet for now).

The above figures are rolling 3 year sums so we should divide by three to get rolling three year averages.

According to that, CCH is trading now at a 6.9% free cash yield versus EV using the past three years.

That basically means that if you spent 6.6 billion Euros to buy the entire company and pay down their debt, your cash-on-cash return on this investment would be

6.9% if CCH earned the same revenues/profits as they did in the past three years. (Importantly, this differs from EV/EBITDA as it deducts taxes paid and capex; so the 6.9% would actually end up in your hands).

Using the CCH forecast for the 2010-2012 period, they expect cash flow to be 1.4 billion Euros over the three years frmo 2010 to 2012. That comes to 467 million Euros per year and a free cash yield on EV of 7.1%.

Let's look at this from an equity investor point of view. I will just deduct 83 million Euros from the above free cash figures and compare that to the equity market valuation (or on a free cash per share basis). 83 million Euros is what financing cost was in 2010 and for the first nine months of this year, it seems to annualize to the same run rate.

So using 83 million, then the free cash flow for the past three years was 370 million Euros (1.36 billion divided by three minus 83 million). With around 366 million shares outstanding, that comes to around 1.00 Euro per share.

To make it easy to compare to the ADR, let's call that U.S. $1.35/share. At $15.30/share, CCH is trading at a free cash flow yield of

8.8%.

Using guidance from the presentation and doing the same calculation gives you 384 million Euros or $1.42/share, or a free cash yield of

9.3% which is not bad at all given current bond yields out there.

The most interesting aspect of this, still, is the cheapness especially relative to the growth potential.

Obviously, Europe is not at all out of the woods and there will be a lot more volatility in the financial markets going forward and CCH has exposure to a lot of the 'wrong' places in the current environment, so it wouldn't be much of a surprise if this stock went down a lot more on the daily headlines.

But if you assume that CCH doesn't require a bubble to make good returns and grow (this is not a housing stock or a bank, for example, that benefited greatly from the bubbles), then it is reasonable to assume that they can resume their growth and make decent money going forward in a more normalized environment.

In any case, if you are looking for something in Europe from this crisis, some will make some money buying European bank stocks and other more levered played (if they are right).

This one looks like a more conservative way to play that.

There is good reason to assume that CCH might be oversold due to their being a Greek company; Even if Greece defaults, it will not have an impact on CCH's credit rating; both S&P and Moody's have affirmed that as most of CCH's business is outside of Greece.

Plus, even if Greece does default and there is a blowup over there, solid companies with good businesses should come through fine, as many companies have done in the various blowups over the years in South America (oftentimes, blowups or times of near blowups have been the best times to buy into their stock markets! You want to buy when everyone is running away).

There is a risk, however, in that most of their debt is denominated in Euros and U.S. dollars; if the Euro completely breaks up, the 'new' Euro may be the strong core countries and therefore it would be very expensive versus the rest of the currencies. CCH does have a lot of sales in the European countries that are not big and strong (France and Germany). However, many of the smaller countries CCH serves is not in the Euro so foreign currencies declines are already in the numbers.

A breakup of the Euro, for this reason would be hugely traumatic to Europe overall so is probably highly unlikely in the near future. One mitigating factor is that if there is a breakup of the Euro, weaker currency economies will see high inflation so the loss from the foreign currency revenues would be partly made up by higher prices in those countries.

I don't own any at the moment and I will be looking at this more and I may buy some at some point. Even if I don't buy some now, at the very least will go into my "watch very closely" list.