Anyway, some of my favorite annual reports are out, so I thought I'd use that as an excuse to break the silence and try to get back into posting more regularly.

The JPM report, as usual, is really well written. I see a lot of people have a lot to say about it and I guess that's good, that it gets attention and gets people talking about the various issues.

I noticed Cramer saying that Dimon is whining too much and that he should admit and talk about all the things that JPM has done wrong and not just criticize regulations/policy. To be fair, Dimon has talked a lot about what JPM and the industry has done wrong over the years, often in real time. He has been doing that for years, so it's not like he hasn't taken responsibility for a lot of what's coming at the industry these days.

But I do agree that a lot of this stuff (anti-corporate, anti-big-bank rhetoric) seems to be going overboard. As usual, people tend to expend a lot of energy fighting the last battle (and missing what's coming next!).

Anyway, enough of that. Let's take a look at some cool charts.

Performance

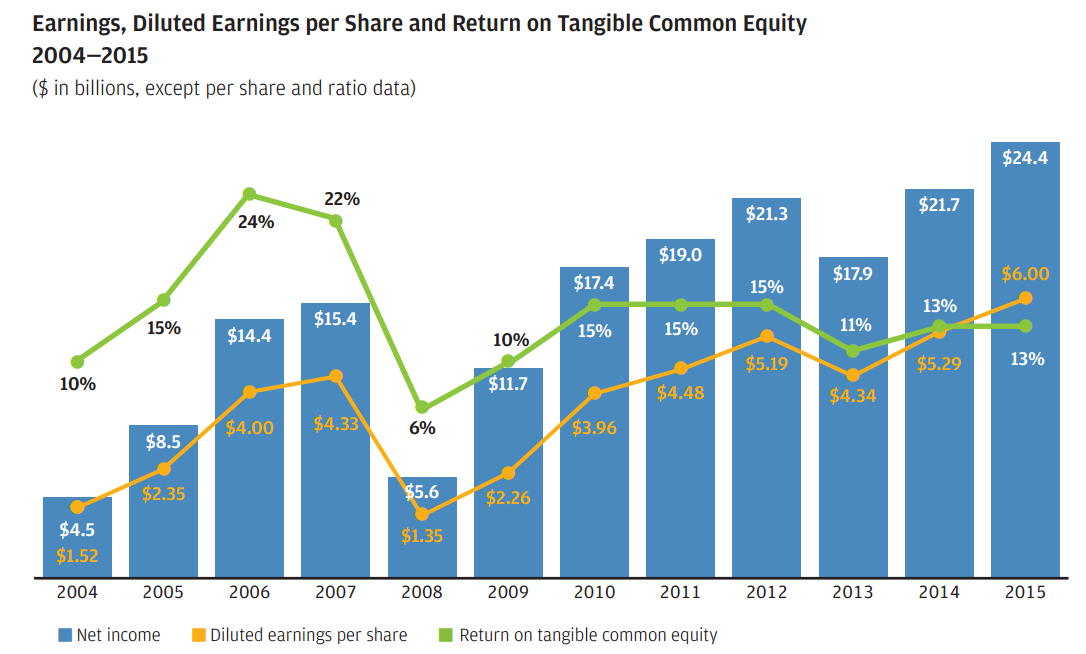

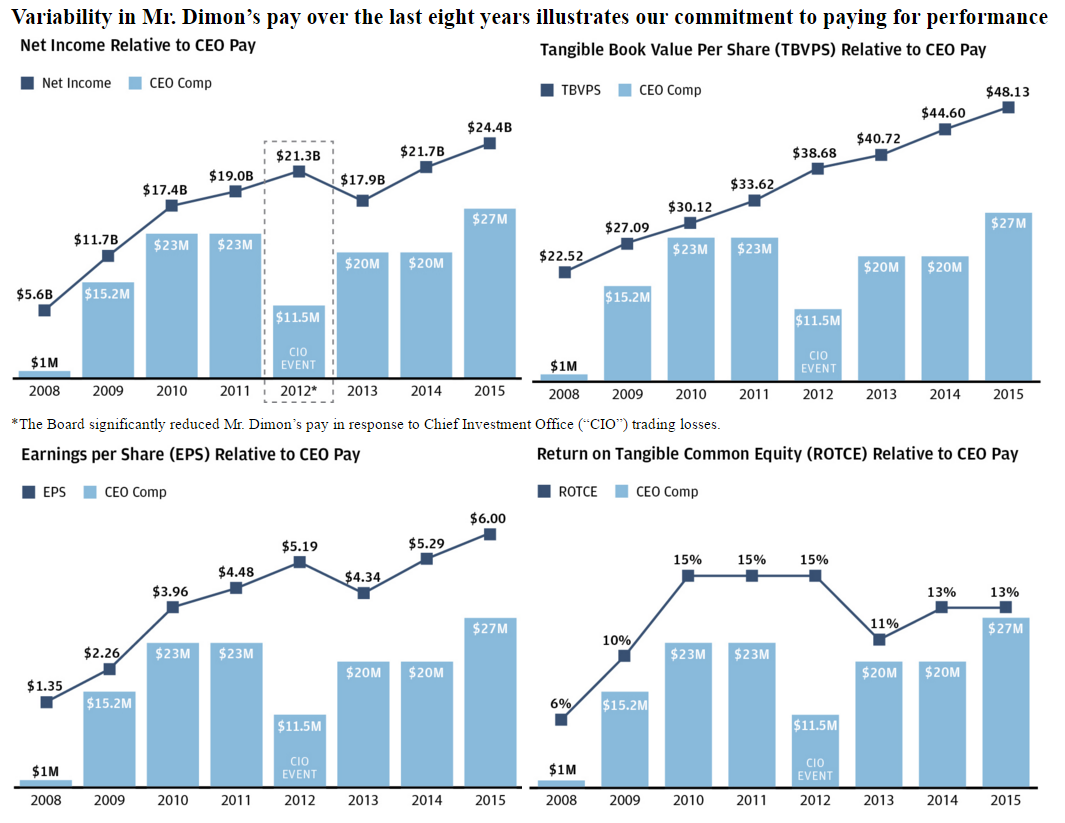

Dimon's letter is full of great charts. I wish more annual reports were like this. But then again, if you don't have a great historic track record, you wouldn't want charts like these in the first few pages of your report.

For many years since the crisis, people kept saying that JPM is putting up fake profits by reversing loss reserves and that when that runs out their earnings will tank. Or that spread compression will continue so their earnings will tank on that. Or that increasing capital requirements will hit their earnings. Well, they've been saying these things for years but JPM made record profits again in 2016.

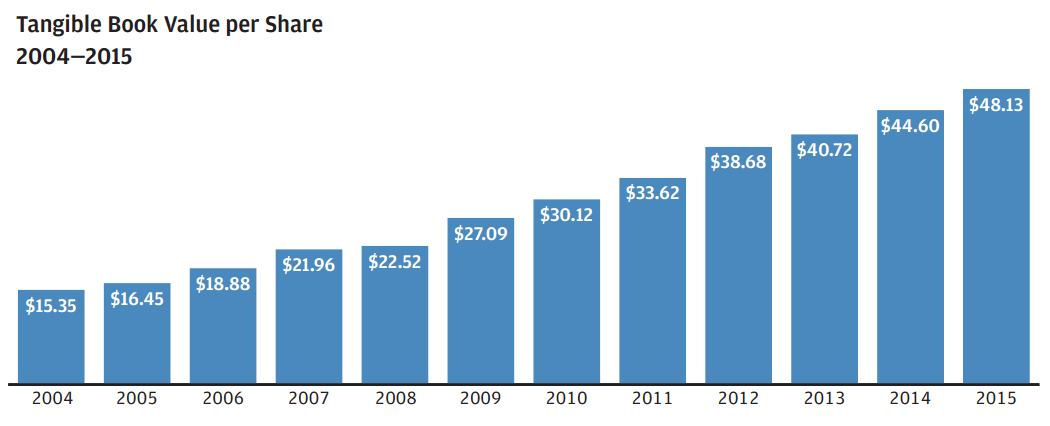

And tangible book value per share has been rising every year since 2004. Since the 2007 peak, TBPS has increased 10.3%/year. That's pretty astounding. This includes the great recession/ financial crisis, and the Whale 'disaster'.

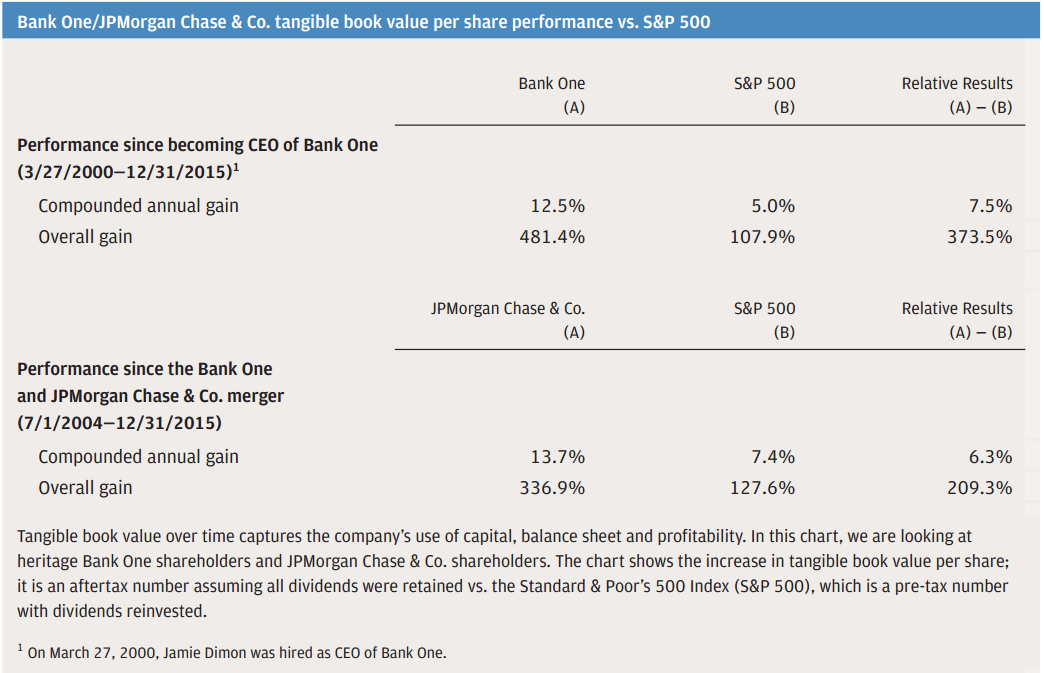

TBPS has outperformed the S&P 500 since Dimon became CEO of Bank One, and since the Bank One/ JP Morgan merger.

Total return of the stock hasn't been as great, though. But a CEO can't really control the stock price.

Dimon regrets that the stock price, while outperforming the industry, has only kept pace with the S&P 500 index.

Just for fun, and since Dimon and most of us are Buffett fans, I'll compare these figures with Berkshire Hathaway (BRK). This may not be totally fair as I will compare tangible BPS growth of JPM with the BPS of BRK. BRK does have a lot of goodwill on the balance sheet so it will make a difference. So keep that in mind. Still, BRK's BPS growth is a decent benchmark for performance of a great CEO.

First, let's just look at the BPS changes:

JPM BRK

2000-2015 +12.5% +9.2%

2004-2015 +13.7% +9.8%

2007-2015 +10.3% +9.0%

1 year +7.9% +6.4%

5 year +9.8% +10.3%

10 year +7.9% +10.1%

The figures for JPM are from the tables/charts above. The 1, 5 and 10 year figures exclude dividends as I just looked at the TBPS chart. JPM figures start during the year for 2000 and 2004 whereas for BRK, I just used the closest year-end figure (so as to minimize my work-load).

The bold figure is the higher one. You will see that JPM has outperformed BRK in just about every time frame, even from the 2007 high. That's really crazy when you think about it (The five and ten year exclude dividends so is understated).

In 2007, right in front of the worst financial crisis since the great depression, if you knew exactly how bad it was going to get, you would never guess that JPM will outpeform BRK over the next eight years. JPM had trillions and trillions of derivatives exposure, billions of mortgages, investment banking business exposure etc. And BRK was a rock solid winner in bad times with the greatest capital allocator of all time etc.

OK, let's look at the stock price.

JPM BRK

2000-2015 +10.2% +8.2%

2004-2015 +7.6% +7.6%

2007-2015 +7.8% +4.3%

1 year +8.4% +1.4%

5 year +12.1% +10.4%

10 year +7.9% +8.3%

By stock price, JPM outperforms in just about every time frame too. This one doesn't have the tangible BPS versus BPS problem, so is 'pure' in that sense. Not bad at all.

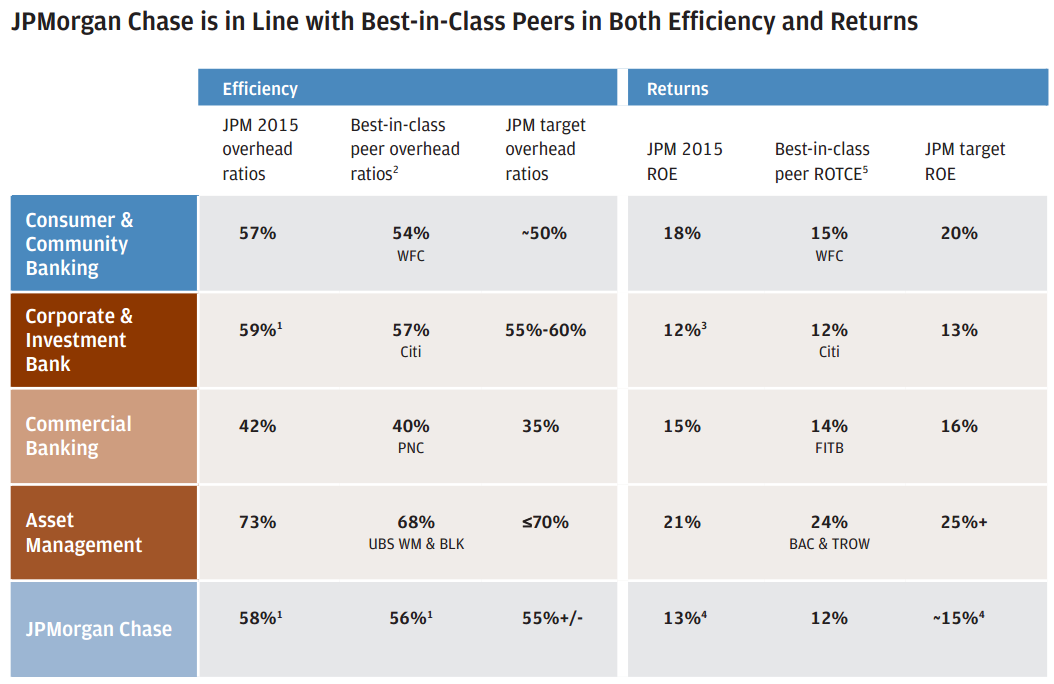

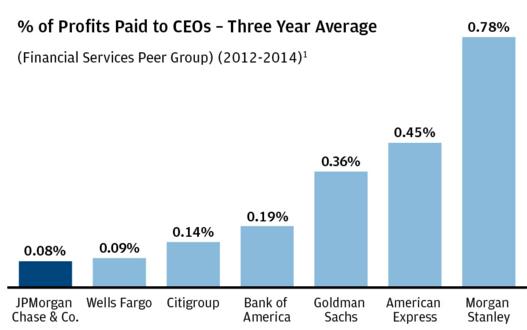

Best in Class Across the Board

And it's not like JPM is doing well in one area versus another. It seems like they perform consistently in all areas, which is reassuring.

Break Up the Big Banks?

Dimon spends some time talking about the big bank issue. You may not agree with everything he says (I do, though... surprised?), but he raises many valid points. The thing that annoys me about this argument is that the biggest problems (well, OK, Citi was a problem) were Lehman, Bear Stearns, Merrill Lynch and Morgan Stanley. Oh, and AIG, which wasn't even a bank or investment bank.

JPM, WFC and even BAC did fine throughout the crisis. Well, BAC got into trouble for what it did during the crisis, but I think they were fine going into it.

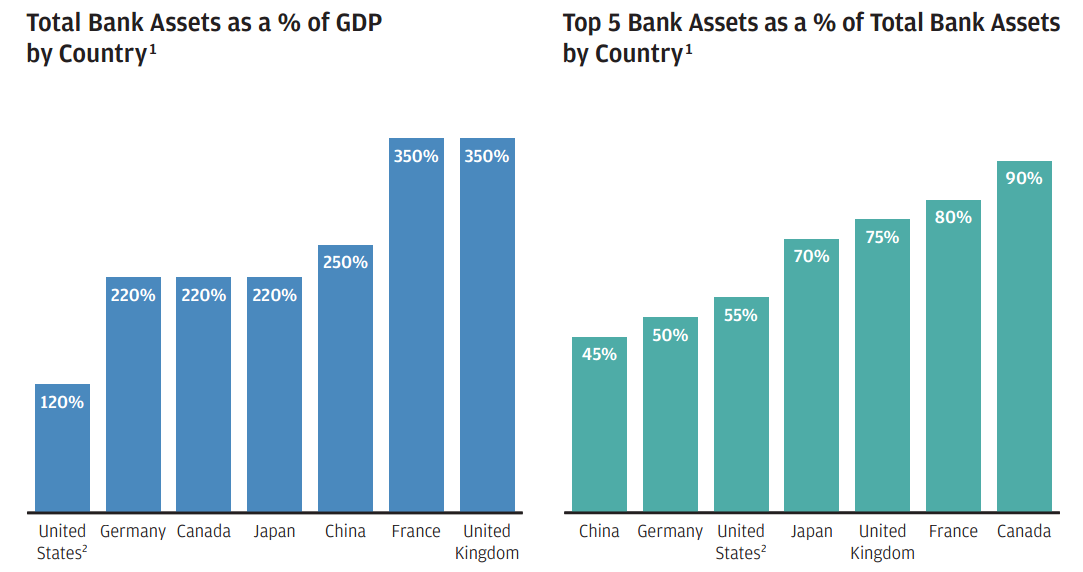

Anyway, here are some interesting charts in Dimon's letter that shows that our big banks aren't even that big, relatively speaking, compared to other countries.

Call me stubborn (or stupid), but I still think Glass-Steagall is not an issue, really. I know many veterans on Wall Street (even the ones that wanted it repealed) believe that Glass-Steagall should be reinstated and that investment banks and commercial banks should be separated.

This has never made any sense to me. If you are a financial services company and have a client that needs to raise funds, why should there have to be two separate entities depending on if you want to borrow money from you (as a bank) or sell bonds to your clients (as an investment banker)?

I remember reading about the old days when institutions were highly regulated, based on things like if you are making long term loans or short term loans, interest rates were regulated etc. In fact, the S&L industry was very highly regulated and they blew up spectacularly. I don't think any one S&L was big enough to threaten the financial system, but they all seemed to blow up at once. Too big to fail? Or too many to fail?

The Solution

Buffett probably has the best answer to all of this; clawbacks and make sure that the CEO ends up in the poorhouse if their bank fails. The fact that the CEOs that blew up their firms during the financial crisis are playing golf at exclusive clubs and are living rich is really annoying even to me (the big financial industry groupie/cheerleader). OK, this has nothing to do with Dimon's letter.

Increasing capital requirements drastically may not matter as many banks that blew up early in the last century had very high capital ratios. Turning banks into utilities, as Dimon says, makes no sense either. Utilities are monopolies, first of all. Banks are not.

Utilities have their own problems, and they've had their own blowups.

Interest Rates

In the letter, Dimon says he is not worried about negative interest rates. He is in fact much more worried about interest rates going up faster than they expect. And in the Goldman Sachs letter, Blankfein/Cohn say, "We don't see how a world of zero or negative interest rates could possibly be the 'new normal'".

To which I say, "but what if it is!!??!".

That would be my big fear for financial stocks. We have all been watching the impossible happen, first in Japan, and now in Europe. Yes, we are better here for sure. But how much better? Can we really avoid this 'new normal' if it continues in Japan/Europe etc.? Are we strong enough to resist such a strong force? Even the strongest swimmers will drown if weighed down by an anchor heavy enough... I don't know.

Anyway, the letter is a great and educational read so go read it!

By the way, there is a shareholder proposal in the proxy. But before that, let's take a look at some charts from it.

So Dimon's pay is performance based, and we are getting a great deal.

Anyway, here is the proposal:

Proposal 7Appoint a stockholder value committee — address whether divestiture of non-core banking business segments would enhance shareholder value

Bartlett Naylor, 215 Pennsylvania Avenue, S.E., Washington, D.C. 20003, the holder of shares of our common stock with a market value in excess of $2,000, has advised us that he intends to introduce the following resolution:

Resolved, that stockholders of JPMorgan Chase & Co. urge that:

And here's the supporting info:

The financial crisis that began in 2008 revealed that some banks were “too big to fail.” This is the moral hazard that invites managers to take extraordinary risks with an understanding that taxpayers will rescue the firm, as failure would cause widespread financial chaos. That 2008 rescue may have served JP Morgan’s creditors, but shareholders suffered. JP Morgan stock fell from $49.63 on Oct 1, 2008, to $15.93, on March 6, 2009.

Risk-taking at major banks can be especially lethal following the elimination of certain activity restrictions (known in the vernacular as “Glass-Steagall”) on how a bank can deploy FDIC-insured deposits. Congress began to address some of these problems with the 2010 Dodd-Frank Act. But an analysis by Goldman Sachs argues that implementation of this law means JP Morgan would be worth more in parts.

The crisis and subsequent events have also demonstrated that JP Morgan may be “too big to manage.” Mismanagement of deposits by a half-dozen London-based traders (known as the “London Whale”) sent JP Morgan stock down 24 percent. Further, shareholders have paid more than $30 billion in fines because bank managers failed to prevent misconduct in a variety of operations.

We therefore recommend that the board act to explore options to split the firm into two or more companies, with one performing basic business and consumer lending with FDIC-guaranteed deposit liabilities, and the other businesses focused on investment banking such as underwriting, trading and market-making. Divestiture would also give investors more choice and control about investment risks.You can go read JPM's response to this, which is good. But what I was thinking as I read this was:

- Well, the stock price declined a lot, but JPM didn't lose money in any single quarter throughout the crisis! Look at the charts in the letter to shareholders. There is not even a blip where the financial crisis occured (in terms of TBPS).

- My old-fashioned thinking is that Glass-Steagall's elimination can't be the cause of the crisis because the biggest problems occurred at independent investment banks. In fact, GS, MS and others wanted to become attached to banks to enhance stability; this is exactly the model at JPM, and that is why JPM was so stable throughout the crisis. Citibank had problems, but that's a whole other story, I think.

- The London Whale trade made the JPM stock price go down, but it was pretty inconseqential, relatively speaking (loss versus shareholders' equity etc.). Ironically, in hindsight, it's basically a tempest in a teapot...

- JPM paid $30 billion in fines, but other firms paid a lot of fines too. GS, MS and others paid fines too because "managers failed to prevent misconduct in a variety of operations".

Anyway, as it says in the proxy, JPM has described at their investor days in the past few years why the integrated model makes sense.

OK, so that wasn't so hard (to make a blog post after three months!).